ASIC’s Crackdown on Private Credit: What It Means for Investors

Simon Turner

Mon 30 Mar 2026 6 minutesIn recent years, private credit has emerged as a mainstay source of income for many investors, particularly retirees. In an environment defined by persistent inflation, increasingly volatile equity markets, and rising interest rates, some investors have been increasing their exposure to private lending strategies offering yields of 7 to 10% or more.

This rapid growth has not gone unnoticed by the regulator. In recent months, ASIC has sharpened its focus on private credit, signalling what may prove to be a defining moment for the asset class.

A Mainstream Asset Class with Extraordinary AUM Growth

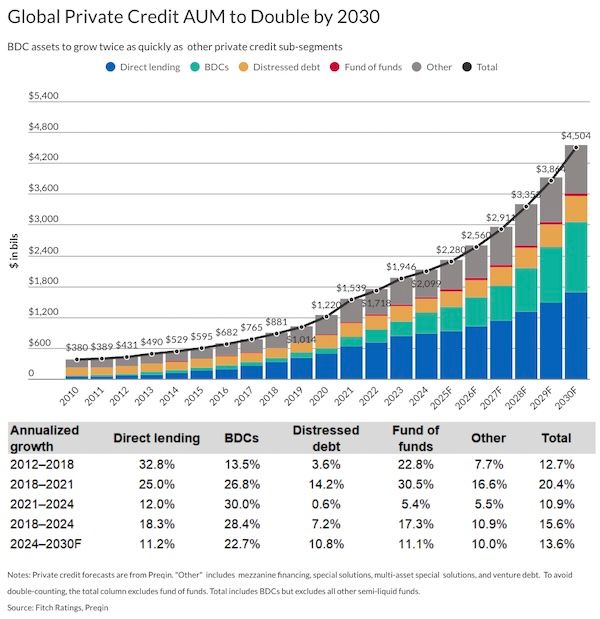

All this matters because the growth in private credit assets under management (AUM) has been extraordinary. AUM has more than doubled over the past five years, surpassing US$2.3 trillion globally. Moreover, it is expected to double again by 2030.

The Australian private credit sector is following a similar trajectory, with most domestic managers expanding aggressively in recent years into real estate lending, corporate direct lending, and structured credit.

The domestic appeal has been compounded by the banking sector’s retreat. As the banks have retrenched from certain forms of lending due to regulatory capital constraints, the private lenders have stepped in, often at higher margins.

In short, it’s important to understand that ASIC’s intervention is coming at a time when the sector is booming.

Explore 100's of investment opportunities and find your next hidden gem!

Search and compare a purposely broad range of investments and connect directly with product issuers.

ASIC’s Concerns

ASIC has genuine concerns about private credit.

In its recent updates, it has warned that ‘the rapid expansion of private markets, including private credit, presents heightened risks for retail investors, particularly where transparency is limited and valuation practices are complex’.

ASIC is essentially recognising that, as capital has flooded into the asset class, the risk has shifted from credit quality to the structure and governance of the vehicles themselves.

As Patrick William, Managing Director of Rixon Capital’s Income Fund and Credit Opportunities Fund explains: ‘The challenge with existing regulation is that the rules were written for listed equity. Private credit differs on two key fronts. First, debt returns are prescribed; i.e. x% p.a. Second, debt is nuanced. First ranking or subordinated? Where do you generate fee income? ASIC sees risk in fund marketing on the basis of returns without adequately communicating underlying risk.’

ASIC’s actions are clearly pre-emptive in addressing any downside scenarios, with the intent of strengthening the system before financial stress emerges.

With this goal in mind, it has indicated its intention to increase surveillance of private credit fund marketing practices: ‘disclosure must be clear, balanced and not misleading, especially where higher returns are being promoted in a low growth environment’.

ASIC’s concerns extend to the inherent liquidity mismatch observed when investors seek to exit a private credit fund en masse.

Patrick takes a more favourable view of the sector on this front, noting: ‘Private credit illiquidity is stated on the box – hence the private. An allocation in private credit is meant to be a medium-to-long-term investment, not a trade.’

Of course, investors should be aware of this when considering the asset class. Many private credit funds offer periodic liquidity, yet the loans themselves are inherently illiquid. So, in times of stress, this mismatch can lead to gating and delayed withdrawals.

Having said that, the risk of forced asset sales to fund redemptions is low in the Australian market. ASIC RG136 requires that responsible entities maintain liquidity management policies ensuring redemptions do not materially disadvantage remaining investors. Hence, the obligation to suspend redemptions when assets cannot be sold without a significant discount is built in.

As Patrick concludes: ‘Investors are compensated for this via an illiquidity premium of several percent.’

Investor Takeaways

For investors, the implications are nuanced:

- Due Diligence and Manager Selection More Important Than Ever

ASIC’s scrutiny is surely a signal that differentiation within the sector is becoming increasingly important.

High-quality managers with disciplined underwriting, conservative loan-to-value ratios, and transparent reporting are likely to emerge stronger.

In contrast, those relying on aggressive structures or opaque strategies may face greater pressure.

Hence, investors should focus on funds that provide detailed reporting on loan exposures, sector concentrations, and credit quality.

They should also focus on funds with liquidity/redemption features which are consistent with the nature of the underlying assets.

- Not a Time to Stretch for Yield

Most private credit investors are focused on income, so there’s a strong temptation for managers to stretch for the highest possible yield.

However, this can lead to weaker underwriting standards and greater risk-taking than investors may be aware of.

In the face of the risks ASIC has highlighted, now is arguably the time to prioritise fund managers with proven track records and conservative approaches rather than the highest yield in the sector.

- Stress Test for Higher Rates

It’s important to remember that private credit has flourished during a period of relatively benign credit conditions. Default rates, while rising modestly in recent months, remain below long-term averages, so most investors have been receiving their distributions year in, year out.

However, if interest rates continue rising and refinancing pressures build, particularly in commercial real estate, the next phase of the cycle may test the resilience of these portfolios.

It’s probably prudent to prepare for that less benign part of the cycle right now.

As a result, it’s time to stress test private loan portfolios for higher rates, or at least, to focus on private credit managers who are actively stress-testing and preparing for tougher market conditions.

- Recognise the Potential Upsides of ASIC’s Intervention

ASIC’s recent attention on private credit is not inherently negative.

Historically, periods of increased regulatory oversight of various asset classes have often led to stronger, more resilient markets.

So, ASIC’s crackdown may ultimately enhance the credibility of private credit as an asset class, particularly for retail investors. At the very least, their actions are inspiring more discussion like this, and growing investor awareness of the risks of investing in private credit. Used prudently, that’s likely to help rather than hinder investors’ private credit returns.

Subscribe to InvestmentMarkets for weekly investment insights and opportunities and get content like this straight into your inbox.

Focus on Best-in-Class Funds

Best-in-class private credit funds, which emphasise secured lending and active risk management, may well benefit from this regulatory-driven shift towards higher standards. They will distinguish themselves through superior communication on these issues, including disclosure of their portfolio stress-testing.

The key takeaway is that due diligence of prospective funds is more important than ever. As ASIC says: ‘investors should carefully consider whether the risks of private market investments align with their financial objectives and risk tolerance’.

Having said that, private credit funds remain compelling for their income generation, particularly in diversified portfolios where they can complement fixed income and equities. Just make sure you give it enough thought and analysis prior to investment.

Funds Mentioned

Disclaimer: This article is prepared by Simon Turner. It is for educational purposes only. While all reasonable care has been taken by the author in the preparation of this information, the author and InvestmentMarkets (Aust) Pty. Ltd. as publisher take no responsibility for any actions taken based on information contained herein or for any errors or omissions within it. Interested parties should seek independent professional advice prior to acting on any information presented. Please note past performance is not a reliable indicator of future performance.

Simon Turner is an ex-fund manager with 20 years investing experience gained at Bluecrest, Kempen and Singer & Friedlander who now writes educational content about investing and sustainability. He's also the published author of The Connection Game and Secrets of a River Swimmer.