What is a Diversified Income Fund?

Diversified income funds are managed investment funds that allocate capital across several income producing asset classes to generate regular distributions for investors.

These funds typically combine:

- Fixed income securities such as government and corporate bonds;

- Floating rate notes issued by banks and financial institutions;

- Property debt and mortgage-backed investments;

- Private credit and alternative income strategies;

- Dividend paying equities and infrastructure assets.

The goal is to produce consistent income while limiting exposure to any single risk factor.

Unlike traditional bond funds or equity income funds, diversified income funds use a multi-asset approach to income generation.

This diversification across asset types, geographies, and credit qualities provides more stable income than single-asset funds, particularly during periods when one asset class underperforms.

Fund managers dynamically allocate capital based on market conditions, yield opportunities, and risk management principles, making these funds suitable for income-focused investors, retirees, and SMSFs who want regular distributions without managing individual securities.

Morningstar highlights that diversified multi asset income portfolios can help reduce income volatility by combining assets that respond differently to economic cycles. As a result, diversified income funds have become increasingly popular with investors seeking reliable portfolio income.

These funds differ significantly from alternatives in the Australian market.

Bond funds invest exclusively in fixed income securities, property funds concentrate on property or property debt, and equity income funds hold only dividend-paying shares.

Diversified income funds combine multiple income sources, reducing concentration risk. If corporate bond defaults rise during a recession, the fund’s government bond and cash holdings help stabilise returns. When property markets weaken, floating rate notes and corporate bonds can offset losses.

This multi-asset approach provides defensive characteristics while targeting yields above traditional cash deposits.

Why Income Investing Is Growing in Australia

Income investing is a core strategy for many Australian investors.

Several structural factors are driving this strong demand:

1. Australia’s ageing population

Australian Institute of Health and Welfare data shows that Australians aged over 65 now represent 16% of the population and this proportion continues to grow over time.

Source: The Senior

Retirees increasingly need reliable income streams to replace employment income.

2. Rising interest rates

After a decade of near zero interest rates globally, the RBA cash rate has risen significantly since 2022.

Higher rates have increased yields across fixed income markets, making diversified income funds more attractive.

3. SMSF demand for income assets

The Australian Taxation Office reports that self-managed super funds collectively manage more than $900 billion in assets.

Income generating investments are particularly important during pension phase where regular distributions support retirement income.

How Do Diversified Income Funds Work?

Income Generation and Distribution Mechanisms

Diversified income funds produce distributions from multiple sources:

The distribution process follows a systematic cycle. During the collection phase, fund managers collect all income from underlying assets throughout the period. The deduction phase sees management fees, administration costs, and operating expenses deducted from gross income. In the calculation phase, net income is divided by the number of units on issue to determine distribution per unit. Finally, during the payment phase, distributions are paid to unitholders based on units held on the record date.

Distribution frequency is an important consideration. Most diversified income funds pay monthly or quarterly distributions, with monthly income funds particularly suited to retirees needing regular cash flow. Some funds pay semi-annually or annually, more common when underlying assets are less liquid.

Distribution amounts typically vary each period based on actual income received from underlying assets, interest rate changes affecting bond income, credit performance (defaults reduce income), and fees and expenses. Funds may have distribution targets such as ‘RBA cash rate plus 3% p.a.’ but these are objectives, not guarantees.

Some distributions may include return of capital components, which means returning part of your original investment rather than true income. While not immediately taxable, return of capital reduces your cost base for capital gains tax purposes. High proportions of return of capital may indicate distributions are unsustainable from income alone, warranting closer scrutiny of the fund's underlying earnings.

Distribution Reinvestment Plans are offered by most funds, allowing distributions to automatically purchase additional units. Benefits include compound returns, no transaction costs, and automatic reinvestment discipline. However, you still pay tax on distributions even if reinvested, which increases your cost base. Investors can typically switch between cash distributions and reinvestment as needs change throughout different life stages.

Fund Structure and Management

Diversified income funds operate as registered managed investment schemes regulated under the Corporations Act 2001, providing investor protection through ASIC regulatory oversight and compliance with fund constitution rules.

When you invest, you purchase units in the fund, similar to buying shares in a company but representing a proportional interest in pooled assets. Each unit represents an equal share of the fund's total assets, with unit prices calculated regularly based on Net Asset Value: total assets minus total liabilities divided by the number of units on issue. Pricing frequency varies depending on underlying asset liquidity; daily for funds holding listed securities, weekly or monthly for funds with less liquid property debt or private credit.

Licensed fund managers make all investment decisions on behalf of unitholders without requiring approval for individual transactions. Active management involves continuously monitoring and adjusting the portfolio through market condition assessment (interest rate environment, yield curves, credit spreads, economic outlook), credit quality analysis (assessing default risk, reviewing financial statements, monitoring credit ratings), yield opportunity identification across sectors and credit qualities, liquidity management to meet redemption requests without distressed selling, and portfolio rebalancing when allocations drift from targets or opportunities arise.

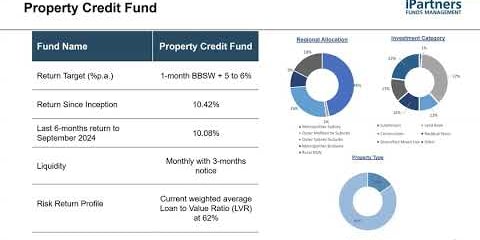

For example, Affluence Income Trust (AIT) is a highly diversified portfolio of fixed income assets that aims to provide investors with a minimum distribution equal to the RBA Cash Rate plus 3% per annum paid monthly over rolling 3-year periods after payment of distributions.

Fund managers often employ two complementary approaches:

- Strategic allocation establishes long-term target allocations based on the fund's stated investment objective, such as 50% bonds, 30% property debt, and 20% cash. These rarely change and provide the portfolio's structural foundation.

- Tactical allocation allows short-term deviations to capture market opportunities, such as temporarily increasing cash holdings if credit spreads are tight and offer poor value, then rotating into corporate bonds when spreads widen and compensation for credit risk improves.

Asset Allocation and Diversification Approach

A typical diversified income portfolio may resemble the following allocation.

Fixed income investments form the core of most diversified income fund portfolios. Australian and international government bonds, issued by sovereign governments and backed by taxing power, provide the lowest risk fixed income exposure. These highly liquid securities offer stability during equity market downturns but pay lower yields than other bond categories. Semi-government bonds issued by state and territory governments provide slightly higher yields than Commonwealth bonds with minimal additional risk, benefiting from implicit government backing and highly rated, liquid markets. Corporate bonds issued by companies to fund operations or expansion offer yield enhancement over government bonds, with risk reflecting issuer creditworthiness. Investment grade bonds rated BBB- or above carry lower risk and yields, typically issued by large established companies, while sub-investment grade bonds rated BB+ or below offer higher yields at higher risk from smaller or more leveraged issuers.

Floating rate notes deserve particular attention in the current environment. These debt securities adjust interest payments periodically, usually quarterly, based on benchmark rates like the Bank Bill Swap Rate. If BBSW is 4% and an FRN pays BBSW plus 1%, the distribution is 5%; if BBSW rises to 5%, payments increase to 6%. This structure protects against rising interest rates, making FRNs popular with banks and financial institutions and valuable during periods of monetary policy tightening.

Hybrids and subordinated debt combine features of both debt and equity, including bank hybrids like ASX-listed PERLS and capital notes issued by major banks to meet regulatory capital requirements, and corporate hybrids issued by companies for flexible financing. These securities offer higher yields than senior bonds as compensation for subordination in the capital structure. They rank lower in repayment priority than senior bonds if issuers default and may include payment deferral rights or conversion to equity. In bank failures, hybrid holders can lose capital before depositors or senior bondholders, requiring careful credit assessment.

Property debt provides yield enhancement over traditional bonds and access to property returns without direct ownership. Funds may allocate to property debt including mortgage funds australia, commercial property loans, and development finance. First mortgages carry first-ranking claims on property if borrowers default, while second mortgages hold subordinate claims with higher risk and higher yields. Commercial property loans are secured by office, retail, or industrial property, while construction finance funds property development in stages and development finance covers land acquisition, subdivision, and infrastructure. These investments are less liquid than listed bonds but offer attractive yields when structured with appropriate loan-to-value ratios—lower LVRs indicate less risk.

Private credit encompasses direct loans to businesses not available through public bond markets, including asset-backed securities, trade finance, equipment leasing, invoice financing, and business loans. Typically available only to wholesale investors, private credit is illiquid and cannot easily be sold before maturity. Higher yields compensate for illiquidity and the sophisticated credit analysis required. Fund managers with established private credit expertise can access attractive risk-adjusted returns unavailable to retail investors directly.

Income-producing equities round out many diversified portfolios, including high-dividend shares from banks, utilities, and telecommunications companies, A-REITs providing exposure to commercial property, and infrastructure securities like toll roads, airports, and utilities. These holdings are more volatile than fixed income but provide both income and potential capital growth. Australian shares deliver franking credits that add tax benefits for eligible investors, though dividends can be cut if company profits decline.

Geographic diversification varies by fund strategy. Most diversified income funds focus on Australian dollar-denominated assets, typically 70 to 100% of portfolios. Some include international fixed income, particularly developed market government and corporate bonds, for additional diversification.

Currency hedging manages foreign exchange risk on international holdings, reducing currency volatility but costing typically 0.2 to 0.6% p.a. Some funds are explicitly currency-hedged as stated in their name or Product Disclosure Statement, while others remain unhedged based on the fund's view on currency movements and investor base requirements.

Key Risks to Consider

While diversified income funds offer valuable benefits, investors must understand the risks inherent in these investments.

Interest rate risk affects all fixed income investments. When interest rates rise, bond prices typically fall, potentially reducing the fund's net asset value. Funds holding longer-duration fixed-rate bonds face greater interest rate sensitivity than those focused on short-term or floating rate securities. Understanding a fund’s duration profile helps assess this risk.

Credit risk arises from the possibility that borrowers default on their obligations. Corporate bonds, property debt, and private credit carry credit risk reflecting borrower financial health. Investment grade bonds have lower default probabilities than sub-investment grade bonds, but defaults can occur across the credit spectrum during economic downturns. Fund managers mitigate this through diversification across borrowers, sectors, and credit qualities, combined with ongoing credit monitoring and analysis.

Liquidity risk becomes relevant when funds hold less liquid assets like property debt or private credit. While daily unit pricing provides investor liquidity, the underlying assets may not be quickly sellable without price concessions. During periods of market stress or high redemption requests, funds may need to sell liquid holdings first, potentially altering the portfolio's strategic allocation. Some funds employ liquidity gates or redemption queues during extreme circumstances, though this is uncommon in well-managed diversified income funds.

Market risk affects income-producing equities within diversified portfolios. Share prices fluctuate based on company performance, sector trends, and broader market sentiment. While equities provide growth potential and franking credits, they introduce volatility. Funds with higher equity allocations will experience greater unit price fluctuations than those focused primarily on fixed income.

Distribution variability means income payments can change between periods. Unlike term deposits with fixed returns, fund distributions fluctuate based on underlying asset performance, interest rate changes, credit events, and portfolio positioning. Investors expecting stable income should review a fund's distribution history and understand the factors that may cause variations.

Counterparty risk exists in derivatives, currency hedging, and repurchase agreements. Fund managers use derivatives for risk management or tactical positioning, creating exposure to counterparty creditworthiness. Reputable funds limit counterparty exposure through diversification and only transact with highly rated institutions.

How to Compare Diversified Income Funds

Comparing funds requires examining multiple dimensions beyond headline distribution rates. Important factors include:

Start with distribution history and consistency. Review the past three to five years of distributions to identify stability or significant variations. Examine whether distributions include return of capital components and if so, what proportion. Funds with consistent distributions predominantly from income demonstrate sustainable operations.

Asset allocation and portfolio composition reveal the fund's risk profile. Examine the breakdown between defensive assets like government bonds and cash versus higher yielding but riskier assets like sub-investment grade bonds, property debt, and equities. Understand geographic exposures and currency hedging policies. Funds with 80% government bonds and cash will behave very differently from those with 50% property debt and private credit.

Credit quality matters significantly. Review the proportion of assets rated investment grade versus sub-investment grade or unrated. Understand the fund's lending criteria for property debt, including typical loan-to-value ratios and security types. Higher-quality portfolios generally deliver lower yields but better stability.

Fee structures directly impact net returns. Compare management expense ratios across similar funds, including management fees, indirect costs, and any performance fees. A fund distributing 5.5% with 0.6% fees may deliver better net outcomes than a fund distributing 6% with 1.2% fees. Watch for entry or exit fees that affect switching costs.

Liquidity terms and conditions vary significantly. Most funds offer daily or weekly redemptions, but some property debt funds may have monthly redemptions or require notice periods. Understand any redemption fees, especially for short holding periods. Some funds impose liquidity gates allowing them to delay or limit redemptions during stressed market conditions.

Fund manager experience and track record provide confidence in ongoing management quality. Research the investment team's experience in credit markets, property lending, or fixed income management. Review commentary in annual reports and distribution announcements to understand management philosophy and market positioning. Funds managed by experienced teams with strong track records through market cycles often justify higher fees.

Minimum investment requirements range from $5,000 for retail funds to $500,000 for wholesale-only strategies. Some funds restrict access to wholesale investors, defined as individuals with net assets exceeding $2.5 million or gross income exceeding $250,000 annually. These restrictions often reflect underlying asset characteristics or regulatory requirements.

Compare funds against relevant benchmarks. While diversified income funds don't track indices, understanding returns relative to the RBA cash rate, bank bill indices, or composite benchmarks helps assess performance. Consistent outperformance net of fees indicates skilled management; consistent underperformance suggests structural issues.

Distribution frequency aligns with income needs. Monthly distributions suit retirees requiring regular cash flow for living expenses. Quarterly distributions work for investors with less frequent income needs or those accumulating wealth through reinvestment. Distribution frequency itself doesn't indicate fund quality but should match your cash flow requirements.

Due Diligence Checklist for Investors

Before investing in diversified income funds, investors should consider the following questions:

- What asset classes does the fund invest in;

- What is the fund’s target distribution yield;

- How liquid are the underlying assets;

- What is the manager’s credit expertise;

- What fees are charged.

Important Tip: Investors should also review the fund’s Product Disclosure Statement and consider whether the strategy aligns with their income objectives.

Who Should Consider Diversified Income Funds?

Diversified income funds suit specific investor profiles and circumstances. Retirees seeking regular income to fund living expenses find monthly income funds particularly valuable. Distributions provide predictable cash flow without requiring security selection or portfolio rebalancing. Professional management reduces the cognitive burden of investment decisions during retirement while diversification across asset classes provides defensive characteristics appropriate for capital preservation objectives. For retirees, funds with high allocations to investment grade bonds, cash, and first-ranking property debt typically offer appropriate risk-return profiles.

Pre-retirees transitioning from accumulation to income phases benefit from gradually shifting portfolios toward income-focused strategies. Diversified income funds bridge the gap between growth-focused accumulation portfolios and conservative retirement portfolios. They provide growing distribution streams while maintaining some capital growth potential through income-producing equities and capital gains on fixed income holdings. Pre-retirees can dollar-cost average into diversified income funds over several years, building positions that will fund retirement income needs.

SMSF investments commonly include diversified income funds, particularly during pension phase when regular distributions fund retirement income. The professional management, diversification, and administrative simplicity make these funds attractive for trustees who want income exposure without directly managing bond portfolios or property debt. SMSF trustees should ensure fund distributions align with pension payment requirements and consider tax implications, particularly franking credits from Australian equities.

Conservative investors prioritising capital preservation over growth find diversified income funds with defensive allocations appropriate. Funds focusing on government bonds, investment grade corporate bonds, cash, and first-ranking property debt provide yields above term deposits with moderate risk profiles. These investors should examine fund volatility, maximum drawdowns during market stress, and recovery periods to ensure risk alignment.

Investors building diversified portfolios use income funds as fixed income allocations replacing or complementing direct bond holdings. Rather than constructing individual bond portfolios requiring minimum investments typically exceeding $50,000 and specialist knowledge, investors access diversified fixed income exposure through managed funds. This works particularly well for portfolio allocations between $10,000 and $500,000 where building diversified direct bond portfolios becomes impractical.

High-income earners seeking tax-effective income may benefit from funds holding Australian dividend-paying shares generating franking credits. Franking credits provide tax benefits for Australian residents, effectively increasing after-tax returns. However, funds with high equity allocations introduce greater volatility, requiring careful consideration of risk tolerance.

Investors should generally avoid diversified income funds when they need complete capital stability with guaranteed returns, making term deposits or government bonds more appropriate. Those with very short investment timeframes under 12 months face potential unit price volatility and may not benefit from diversification. Investors seeking pure capital growth without income requirements would find growth-focused exchange-traded funds (ETFs) or equity funds more aligned with objectives. Finally, those requiring daily liquidity for large positions may find fund redemption processes and potential market impact costs create friction compared to holding listed securities directly.