Why global ETFs matter

Global ETFs matter because Australian investors are no longer using them as niche satellite positions. They are increasingly becoming core portfolio holdings, particularly for SMSFs, advised portfolios and self-directed investors seeking diversified equity exposure outside Australia.

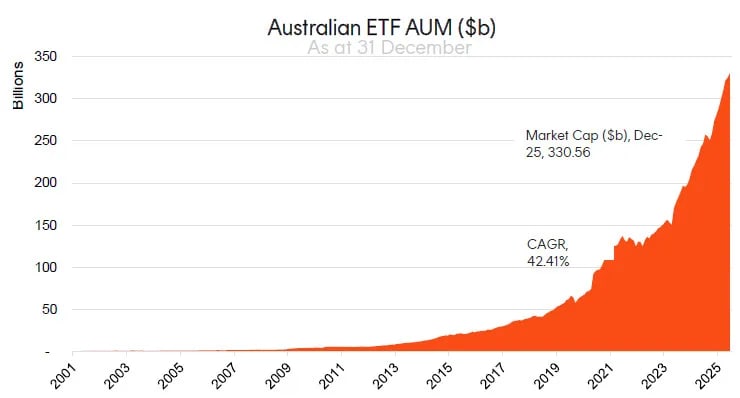

The growth of the Australian ETF market has been striking. Betashares reported that the Australian ETF industry ended 2025 at $330.6 billion in funds under management, up 34.2% year on year. It also reported that international equities ETFs were the largest recipient of net flows in 2025, attracting $20.9 billion.

Source: Betashares

That flow data matters because it tells us something about investor behaviour. Australian investors are increasingly recognising that global markets are not a decorative addition to a portfolio. They are where most of the world’s dominant companies, industries, and innovation cycles are listed.

The MSCI World Index, for example, had a United States weighting of more than 70% as at April 2026. That concentration is both an opportunity and a risk. Investors buying a global ETF may believe they are buying geographic neutrality, when in practice many global equity indices are heavily exposed to US mega-cap companies.

The central issue is not whether global ETFs are useful. They are. The more important question is whether investors understand what they own, why they own it, and how it interacts with the rest of their portfolio.

What is a global ETF?

A global ETF is an exchange traded fund that provides exposure to assets outside Australia, or to a globally diversified asset universe, through a listed vehicle traded on an exchange such as the ASX or Cboe.

In practice, global ETFs can hold international shares, global bonds, listed infrastructure, real estate securities, commodities-related equities, currency-hedged share portfolios, thematic exposures, factor strategies or active global equity portfolios.

MoneySmart describes ETFs as a way to gain exposure to an index or asset class through a fund traded on exchange.

The term global ETF can therefore mean several different things. A broad developed-markets equity ETF is very different from a Nasdaq 100 ETF, a global healthcare ETF, a global infrastructure ETF, a global bond ETF or a copper miners ETF. Each may sit under the global ETF umbrella, but each plays a different portfolio role.

A useful starting distinction is between the eight main categories of global ETFs:

1. Broad Market Global Equity ETFs

Broad market global ETFs are often the foundation of internationally diversified portfolios.

Rather than attempting to select individual companies, these ETFs provide exposure to large groups of businesses across multiple countries and sectors through a single investment.

One of the most widely recognised examples available through InvestmentMarkets is the

SPDR S&P 500 ETF Trust (SPY).

The fund provides exposure to 500 of the largest listed companies in the United States, including many of the world's dominant technology, healthcare and consumer businesses.

For many Australian investors, broad-market ETFs help address a structural issue within the domestic share market. Australia represents only a small percentage of global market capitalisation, and local indices remain heavily concentrated in financials and resources.

International broad-market ETFs provide exposure to sectors such as:

- cloud computing

- artificial intelligence

- semiconductors

- biotechnology

- global consumer platforms

However, investors should recognise that broad-market ETFs are not necessarily diversified in the way many assume. Market-cap weighted indices have become increasingly concentrated in a small number of US mega-cap companies. As a result, many global ETFs now carry substantial exposure to firms such as Microsoft, Apple, Nvidia, Amazon and Alphabet.

Understanding these hidden concentration risks has become an increasingly important part of ETF due diligence.

2. Global Factor and Smart Beta ETFs

Factor ETFs attempt to improve on traditional index investing by targeting characteristics that academic research has associated with stronger long-term risk-adjusted returns.

Examples available through InvestmentMarkets include: iShares Edge MSCI Australia Multifactor ETF (AUMF).

Multifactor strategies typically combine exposures to:

- value

- quality

- momentum

- low volatility

- size

Rather than allocating capital purely according to company size, these ETFs use systematic rules designed to identify businesses exhibiting desirable characteristics.

For sophisticated investors, factor ETFs can serve as a way of introducing more disciplined portfolio construction frameworks while potentially reducing some of the valuation risks associated with heavily concentrated market-cap weighted indices.

However, factor strategies can experience extended periods of underperformance, particularly during environments where speculative growth stocks dominate market returns.

3. Global Sector ETFs

Sector ETFs allow investors to increase exposure to specific industries rather than owning the broader market.

One example available through InvestmentMarkets is BetaShares Global Energy Companies Currency Hedged ETF (FUEL).

FUEL provides exposure to major global energy companies while hedging foreign currency risk back into Australian dollars.

Energy-sector ETFs often behave differently from broad equity indices because returns are influenced by:

- commodity prices

- geopolitical events

- capital expenditure cycles

- energy demand trends

- supply constraints

Another example is: Global X Semiconductor ETF (SEMI).

SEMI provides exposure to semiconductor manufacturers and related technology businesses involved in advanced computing, artificial intelligence infrastructure and digital hardware supply chains.

Semiconductors have become one of the most strategically important industries globally, underpinning everything from AI systems and cloud infrastructure to electric vehicles and industrial automation.

Sector ETFs can offer powerful thematic exposure, but they generally introduce higher concentration risk and greater volatility than diversified market-wide funds.

4. Global Thematic ETFs

Thematic ETFs focus on long-term structural trends rather than traditional industry classifications or geographic allocations.

These funds seek exposure to businesses expected to benefit from transformational changes in technology, demographics or consumer behaviour.

An example available through InvestmentMarkets is BetaShares Video Games and Esports ETF (GAME).

GAME provides exposure to companies involved in:

- video game development

- esports ecosystems

- gaming hardware

- digital entertainment platforms

Another example is Global X Cybersecurity ETF (BUGG).

BUGG focuses on companies providing cybersecurity software, digital infrastructure protection and network security services.

Cybersecurity has evolved from a niche technology segment into a critical component of modern economic infrastructure as governments, corporations and consumers become increasingly dependent on digital systems.

Thematic ETFs can deliver strong returns when the underlying structural trend develops as anticipated. However, they also tend to experience:

- higher volatility

- valuation risk

- sentiment-driven price movements

- greater concentration in a relatively small number of companies

For this reason, many investors use thematic ETFs as satellite allocations around a diversified portfolio core.

5. Income-Focused Global ETFs

Many investors seek international diversification without sacrificing portfolio income.

One example available through InvestmentMarkets is BetaShares S&P Global High Dividend Aristocrats ETF (INCM).

INCM focuses on companies with established histories of maintaining or growing dividend distributions over time.

For Australian investors accustomed to dividend-focused investing, international income ETFs can provide:

- diversification beyond Australian banks

- exposure to global cash-generative businesses

- broader sector representation

- alternative income sources

However, sophisticated investors recognise that yield alone is not necessarily a sign of quality. Understanding dividend sustainability, payout ratios and underlying business economics remains essential.

6. Active Global ETFs

One of the fastest-growing segments of the ETF market is actively managed ETFs.

Unlike traditional passive ETFs that simply track an index, active ETFs rely on investment managers to make portfolio decisions.

Examples available through InvestmentMarkets include Vanguard Global Value Equity Active ETF (VVLU) and JP Morgan Global Research Enhanced Index Equity Active ETF (JREG).

These strategies seek to outperform traditional benchmarks through:

- security selection

- valuation analysis

- portfolio construction expertise

- risk management frameworks

Active ETFs appeal to investors who believe certain market inefficiencies can still be exploited despite the growing popularity of passive investing.

The trade-off is generally higher management costs and the possibility of underperformance relative to the benchmark.

7. Global Fixed Income ETFs

ETF investing is no longer limited to equities.

International bond ETFs provide access to government bonds, corporate bonds and credit markets across multiple regions.

One example available through InvestmentMarkets is iShares Global High Yield Bond AUD Hedged ETF (IHHY).

IHHY provides exposure to higher-yielding global corporate bonds while hedging foreign currency fluctuations back into Australian dollars.

Global bond ETFs can support:

- income generation

- portfolio diversification

- volatility reduction

- defensive positioning

However, investors should understand that high-yield credit ETFs often behave differently from government bond funds and may experience equity-like drawdowns during periods of market stress.

8. Global Alternative and Specialist ETFs

The ETF market has expanded well beyond traditional share market exposure.

InvestmentMarkets also provides access to specialist ETF categories that target alternative return streams and emerging asset classes.

Examples include BetaShares Global Royalties ETF (ROYL).

ROYL invests in companies generating revenue from royalty streams, licensing agreements and intellectual property ownership. These businesses often benefit from scalable business models with relatively low capital intensity.

Another example is 21Shares Ethereum ETF (EETH).

EETH provides listed exposure to Ethereum through an exchange-traded structure, allowing investors to access digital assets without directly managing cryptocurrency wallets.

Investors can also explore technology-focused specialist strategies such as Loftus Peak Global Disruption ETF (LPGD).

LPGD focuses on companies driving technological disruption across industries including cloud computing, communications infrastructure, semiconductors and artificial intelligence.

These specialist ETFs can provide differentiated return drivers and access to emerging areas of the global economy. However, they typically require deeper due diligence around:

- liquidity

- valuation risk

- regulatory uncertainty

- concentration risk

- market structure

The portfolio role of global ETFs

Global ETFs can serve three main roles in an Australian portfolio: diversification, growth exposure and implementation efficiency.

The diversification argument is the most familiar. Australia is a concentrated market. A portfolio dominated by Australian equities is heavily exposed to local financials, resources and domestic economic conditions. Global ETFs can expand the opportunity set to include technology platforms, global healthcare leaders, luxury goods companies, semiconductor firms, industrial automation businesses, global consumer brands and multinational infrastructure assets.

The growth argument is equally important. Many of the world’s highest-quality companies are listed offshore. Investors who want exposure to global earnings growth, innovation, intangible assets and international consumer markets often need to look beyond the ASX.

The implementation argument is more practical. ETFs offer daily liquidity, transparent pricing, simple administration and relatively low minimum investment amounts. On InvestmentMarkets, many global ETFs are listed with minimum investment amounts as low as $1 or $500, depending on the product and issuer.

For a sophisticated investor, however, global ETFs should not be treated as a single asset class. A broad global equity ETF may be a core allocation. A global robotics ETF is a thematic satellite. A currency-hedged global ETF may be a risk-management tool. A global infrastructure ETF may sit somewhere between equities, real assets and income. A global listed private equity ETF may offer access to a specialist return stream, but with equity-market liquidity and listed-market volatility.

The best question is not ‘Which global ETF is best?’ It is ‘What job does this ETF need to do in my portfolio?’

Global ETFs and the limits of Australian home bias

Home bias is understandable. Australian investors know Australian companies, receive dividends in Australian dollars, benefit from franking credits and often feel more comfortable investing in familiar names. But familiarity is not the same as diversification.

A heavy Australian equity bias creates three portfolio issues.

- Sector concentration.

The ASX is structurally tilted towards banks, resources and mature dividend-paying companies. That can be useful for income-oriented investors, but it also narrows the portfolio’s exposure to global growth industries. - Currency concentration.

Australian assets, income, housing wealth, employment income and future spending needs are often already linked to the Australian economy. A portfolio that is also heavily Australian can compound this exposure. - Opportunity cost.

Many industries that define modern equity markets are far larger offshore than in Australia. Semiconductors, cloud computing, global payments, pharmaceuticals, aerospace, luxury goods, software platforms and advanced industrial automation are all more deeply represented outside the domestic market.

Global ETFs help address these limitations, but they can also replace one concentration with another. A global market-cap weighted ETF may reduce Australian concentration while increasing exposure to US mega-cap technology companies. That may be entirely acceptable, but it should be understood.

Active vs passive global ETFs

Passive global ETFs are often appropriate for broad market exposure, while active global ETFs may be more useful where the market is inefficient, concentrated, valuation-sensitive or structurally changing. The decision is not ideological. It should be based on the exposure being sought and the likelihood that active management can add value after fees.

Passive ETFs typically track an index. Their strengths include low cost, transparency, diversification and benchmark consistency. They are particularly compelling in efficient large-cap markets, where many active managers struggle to outperform after fees.

The SPIVA Australia data has repeatedly shown the challenge faced by active managers. In the 2025 scorecard, 70% of active managers in the Global Equity General category failed to match the benchmark’s return for the year, and the 15-year underperformance rate for Global Equity General funds was reported at 96%.

Source: SPIVA Australia

That does not mean active management is futile. It means investors need a high bar. Active global ETFs may be more compelling where the manager has a clearly articulated edge, capacity discipline, a differentiated portfolio, sensible fees and a process that is not merely an expensive version of the index.

InvestmentMarkets’ active ETF listings include global active ETF examples such as the Hyperion Global Growth Companies Fund Active ETF and the Dimensional Global Value Active ETF.

A practical decision framework is worthwhile:

The mistake is assuming either structure is always superior. Passive investing can still produce poor outcomes if investors buy overvalued markets at the wrong time, concentrate unknowingly or panic during drawdowns. Active investing can add value, but only if the manager’s edge exceeds fees, taxes and behavioural friction.

Currency hedged or unhedged global ETFs?

Currency exposure is one of the most important decisions in global ETF investing. It can materially affect returns, volatility and portfolio behaviour.

An unhedged global ETF gives Australian investors exposure to both the underlying overseas assets and the foreign currency movements between those assets and the Australian dollar. If global shares rise and the Australian dollar falls, an unhedged investor may benefit from both equity gains and currency translation. If global shares rise but the Australian dollar rises strongly, some of the gain can be offset.

A currency-hedged global ETF attempts to reduce or neutralise that currency impact, usually by hedging foreign currency exposure back to Australian dollars.

InvestmentMarkets’ currency-hedged global equity section includes examples such as the iShares Global 100 AUD Hedged ETF, which seeks to provide exposure to the S&P Global 100 Hedged AUD Index.

There is no universally correct answer. The case for unhedged exposure is that foreign currency can provide diversification, particularly in global risk-off episodes when the Australian dollar may weaken. The case for hedged exposure is that it can reduce currency-driven volatility and better isolate the underlying asset return.

A sensible approach is to ask three questions.

- What is the asset class? Global bonds are often hedged because currency volatility can overwhelm bond returns. Global equities are more commonly left unhedged, at least partly, because currency exposure may diversify equity risk.

- What is the investor’s spending currency? Retirees spending in Australian dollars may prefer some hedging if they want greater alignment between assets and liabilities.

- What is already in the portfolio? Investors with high Australian-dollar exposure through property, term deposits, Australian shares and employment income may benefit from some unhedged offshore currency exposure.

For many investors, the answer is not hedged or unhedged. It is a blend.

Broad global equity ETFs: the core allocation

Broad global equity ETFs are usually the starting point for investors building international exposure. They provide access to hundreds or thousands of companies across developed markets, or across both developed and emerging markets, depending on the index.

Their appeal is their efficiency. A single ETF can provide exposure to a global opportunity set that would otherwise require dozens of direct shareholdings and substantial research capability. They are often used as the international growth engine of a portfolio.

The main risk is complacency. Broad diversification does not eliminate valuation risk, concentration risk or sequencing risk. A market-cap weighted global ETF will allocate more capital to the largest markets and companies. That means investors buying broad global equities today may still be making a meaningful allocation to the United States and to large technology-related companies. That is not necessarily wrong. It has been a powerful source of return. But it is not neutral in the way some investors imagine.

A sophisticated investor should examine:

This is where an investment research platform can add value. Rather than treating global ETF as a product label, investors can use InvestmentMarkets to compare global ETFs against related categories such as global equity funds, active ETFs, managed funds, global infrastructure, commodities ETFs, hedge funds and diversified funds.

Thematic global ETFs can be useful when they provide disciplined exposure to a structural trend, but they can be dangerous when investors buy a story rather than an investment case.

Thematic ETFs have obvious appeal. Robotics, artificial intelligence, cybersecurity, video gaming, clean energy, defence and ageing populations are powerful narratives. They are easy to understand and often linked to genuine long-term changes in the economy.

InvestmentMarkets includes thematic global ETF examples such as the Global X ROBO Global Robotics & Automation ETF and the VanEck Video Gaming and Esports ETF.

The difficulty is that good themes do not always make good investments.

There are four reasons:

- The theme may already be priced in. A company can benefit from a structural trend and still be a poor investment if expectations are excessive.

- The ETF’s holdings may not match the investor’s mental model. A robotics ETF may contain industrial automation, semiconductor equipment, medical technology and software companies. That may be sensible, but it may not be what the investor expected.

- Thematic ETFs can be narrower and more volatile than broad market ETFs.

- Timing risk is substantial. Investors often discover themes after strong performance has already occurred.

Thematic global ETFs are generally better used as satellite allocations than as core holdings. The question is not whether the theme is real. The question is whether the ETF provides efficient exposure to companies that can convert the theme into durable shareholder returns.

Global infrastructure ETFs

Global infrastructure ETFs can offer exposure to assets such as regulated utilities, toll roads, airports, communications infrastructure, energy infrastructure and transport networks. Their appeal is that some infrastructure assets have inflation-linked revenues, high barriers to entry and long-duration cash flows.

InvestmentMarkets’ ETF listings include global infrastructure-related examples such as the ClearBridge Global Infrastructure Income Hedged Active ETF, which aims to provide income and capital growth from global infrastructure securities while hedging currency exposure back to Australian dollars.

Infrastructure ETFs are not bond substitutes. Listed infrastructure is still equity-market exposed and can fall sharply when rates rise, valuations compress or regulatory risk increases. However, it can play a useful role for investors seeking a blend of growth, income and real-asset characteristics.

For Australian investors, global infrastructure can also diversify away from domestic infrastructure and property exposures. It may complement, rather than replace, unlisted property funds, listed A-REITs, fixed income, private credit or term deposits.

Global listed private equity ETFs

Global listed private equity ETFs provide exposure to listed companies that invest in, manage or hold private equity assets. They can offer a liquid way to access private equity economics, but they are not the same as investing directly in an unlisted private equity fund.

InvestmentMarkets’ global ETF listings include the VanEck Global Listed Private Equity ETF, which is described as providing exposure to a portfolio of the largest and most liquid global listed private equity companies.

The appeal is access. Traditional private equity often involves high minimums, illiquidity, capital calls, complex fee structures and long lock-up periods. A listed ETF structure can make the exposure easier to access and trade.

The trade-off is that listed private equity can behave more like equities than like a smoothing unlisted fund. Its market price can move daily, sometimes sharply, in response to equity markets, credit conditions, valuation multiples and sentiment towards alternative asset managers.

Investors should be clear about the role. A listed private equity ETF may be suitable as a satellite growth allocation for investors who understand equity volatility and want exposure to private markets-related businesses. It is less suitable for investors who assume it will replicate the return profile of an institutional private equity programme.

Global bond ETFs and fixed income considerations

Global bond ETFs can diversify interest-rate, credit and currency exposures, but their risk profile depends heavily on duration, credit quality, hedging and underlying market exposure.

For Australian investors, global bonds are typically used for defensive diversification, income or portfolio ballast. But the label ‘global bond ETF’ is not enough. A short-duration global bond ETF, a long-duration government bond ETF, an emerging-market debt ETF and a high-yield credit ETF are fundamentally different instruments.

Currency hedging is particularly important in fixed income. Because expected bond returns are usually lower than equity returns, currency movements can dominate outcomes if left unhedged. Many Australian investors therefore prefer hedged global bond exposure.

Investors comparing global bond ETFs against InvestmentMarkets’ broader fixed income, private credit and term deposit categories should think carefully about liquidity, capital stability, income reliability and credit risk. Term deposits may offer capital certainty within banking limits, but less liquidity and less market upside. Private credit may offer higher income but less daily liquidity and more credit-specific risk. Bond ETFs offer market liquidity and diversification, but their prices can fall when yields rise.

The right choice depends on the job the defensive allocation is meant to do.

Commodity-linked global ETFs

Commodity ETFs can provide exposure to inflation-sensitive assets, supply-demand imbalances and global resource themes. But investors should distinguish between physical commodity exposure, futures-based exposure and equity exposure to commodity producers.

InvestmentMarkets’ global ETF listings include examples such as the Global X Copper Miners ETF, which provides exposure to copper mining companies rather than to physical copper itself.

That distinction is vital. A copper miners ETF is not the same as owning copper. Mining equities are affected by copper prices, but also by operating costs, political risk, capital discipline, balance sheets, project execution, management quality and equity-market sentiment.

Commodity-linked ETFs are best used with a clear thesis. They may help diversify a portfolio, provide exposure to energy transition demand or act as a hedge against certain inflationary environments. But they can be cyclical, volatile and vulnerable to sharp reversals when supply expectations change.

ETF vs managed fund: which structure suits global exposure?

ETFs are not automatically superior to managed funds. They are simply different structures with different strengths.

ETFs offer exchange trading, usually transparent holdings, relatively low minimums and ease of implementation. Managed funds may offer access to less liquid strategies, capacity-constrained managers, unlisted assets, alternative strategies or structures not easily replicated in an ETF.

For investors using InvestmentMarkets, this distinction is practical. A global ETF may be the right tool for broad international equity exposure. A managed fund may be more appropriate for a specialist global equity manager, private credit exposure, property fund, diversified fund or alternatives strategy.

The structure should follow the strategy, not the other way around.

Liquidity, spreads and trading discipline

ETF liquidity is often misunderstood. The daily trading volume of an ETF is relevant, but it is not the whole story. ETF liquidity also depends on the liquidity of the underlying securities, the role of market makers and the creation-redemption mechanism.

ASIC has warned that ETF spreads can widen in some circumstances, including periods of high volatility or when underlying markets are closed. Market makers are not required to provide bids and offers for 100% of the trading day.

For global ETFs, this matters because the ASX trading day may not overlap with the trading hours of the underlying offshore market. An ETF holding US shares may trade in Australia while the US market is closed. Market makers must price the ETF using futures, currency markets and estimates of fair value. In volatile conditions, spreads can widen.

Practical trading discipline matters.

Investors should generally avoid placing large market orders in thinly traded ETFs. Limit orders are often preferable. Trading near the open or close can be less efficient than trading during more stable parts of the day. For large trades, investors may consider broker support.

The hidden cost of a global ETF is not only its management fee. It is also the bid-ask spread, brokerage, market impact, tax drag and behavioural cost of poor timing.

Tax considerations for Australian investors

Australian investors need to consider both distributions and capital gains when investing in ETFs. The ATO explains that ETF investors may need to include distributions in their tax return and account for capital gains or losses when they dispose of ETF units.

Many ETFs operate under attribution managed investment trust rules, which can attribute taxable components to investors even where cash distributions do not perfectly match the tax components. Investors should use the annual tax statement or AMMA statement provided by the fund issuer and seek professional advice where required.

Global ETFs may also involve foreign income, foreign withholding tax and currency translation considerations. The tax outcome can vary depending on the ETF’s domicile, structure, underlying holdings and distribution policy.

Tax should rarely be the sole reason to choose an ETF, but it can materially affect after-tax returns. This is especially relevant for SMSFs, retirees and high-income investors comparing global ETFs with managed funds, listed investment companies, unlisted funds or direct international shares.

Common mistakes Australian investors make with global ETFs

The most common mistake is believing that a global ETF is automatically diversified. Some global ETFs are broad and diversified. Others are narrow, concentrated or highly thematic.

The second mistake is ignoring currency. A hedged and unhedged version of similar equity exposure can produce materially different Australian-dollar returns.

The third mistake is chasing recent performance. Investors often buy thematic ETFs after a strong run, confusing a compelling narrative with a good entry point.

The fourth mistake is duplicating exposures. An investor may hold a global broad-market ETF, a US ETF, a Nasdaq ETF, a technology ETF and an AI ETF, only to discover that the same mega-cap companies dominate the portfolio.

The fifth mistake is treating ETFs as trading instruments rather than portfolio instruments. ETFs make trading easy. That is not always a benefit. Liquidity can tempt investors into short-term decisions that undermine long-term compounding.

The sixth mistake is comparing fees without comparing exposure. A lower-cost ETF may be better for broad market beta, but fee comparisons are less useful when products track different indices or pursue different strategies.

The seventh mistake is overlooking the Australian context. An Australian investor’s portfolio already includes domestic tax, property, currency, employment and retirement-system exposures. Global ETFs should be assessed against that full balance sheet.

A practical portfolio construction framework

A robust global ETF allocation begins with purpose. Investors should decide whether the allocation is core, diversifying, defensive, thematic or opportunistic.

One useful framework is to divide global ETF exposure into four sleeves:

A conservative retiree may use global ETFs differently from a younger accumulator. The retiree may prefer lower volatility, higher liquidity, some currency hedging and a stronger defensive allocation. The accumulator may accept more unhedged global equity exposure and greater thematic risk.

An SMSF trustee may focus on administration, tax reporting, liquidity and portfolio-level diversification. A high-net-worth investor may combine global ETFs with managed funds, private credit, alternatives, direct shares, property funds and term deposits.

The point is not to find a universal ETF portfolio. The point is to build a coherent one.

How InvestmentMarkets can help investors compare global ETF opportunities

InvestmentMarkets is useful because global ETFs rarely exist in isolation. A global ETF decision often requires comparison with adjacent structures and asset classes.

An investor researching global ETFs may also want to compare:

- Australian ETFs for domestic equity exposure.

- Fixed income funds for defensive allocation.

- Property funds for income and real asset exposure.

- Infrastructure investments for listed and unlisted real asset exposure.

- Private credit for alternative income.

- Hedge funds for diversifying or absolute-return strategies.

- Managed funds for active global equity strategies.

- Term deposits for capital-stable cash allocation.

- Diversified funds for multi-asset implementation.

This cross-category comparison is important because portfolio construction is not a product-collection exercise. It is an exercise in trade-offs. A global ETF may be efficient, liquid and low-cost. A managed fund may offer active judgement. A private credit fund may offer income but less liquidity. A term deposit may offer certainty but limited growth. A property fund may offer yield and real-asset exposure but valuation and liquidity considerations.

The strongest portfolios are built by understanding these trade-offs rather than chasing the most popular product of the year.

Outlook for global ETFs

The outlook for global ETFs is favourable, but not risk-free. Investor adoption is likely to continue because ETFs solve real implementation problems: access, cost, transparency, diversification and liquidity.

However, the next phase of global ETF investing may be more demanding than the last. Investors have benefited from strong US equity returns, rapid ETF product innovation and falling implementation costs. Future returns may depend more on valuation discipline, currency management, diversification beyond US mega-cap technology, and the ability to avoid narrative-driven excesses.

Several themes are likely to shape the market.

First, active ETFs will continue to grow as fund managers use the ETF structure to distribute active strategies.

Second, thematic ETFs will proliferate, making investor discipline more important.

Third, currency-hedged exposures will remain relevant as investors become more conscious of Australian-dollar volatility.

Fourth, global bond ETFs may regain attention as investors reassess the role of fixed income after the rate shocks of recent years.

Fifth, listed access to alternatives, infrastructure, private equity and commodities will continue to blur the line between traditional and alternative allocations.

For sophisticated investors, the opportunity is significant. But the winners will not be those who own the most ETFs. They will be those who use ETFs deliberately.

Limited")