-8c4ntrkc5xpa1bncy14s.jpg)

What Consumer Sentiment Is Telling Us About the Australian Economy

Australian consumers are feeling mighty gloomy right now. It’s easy to understand why. The war in Iran, the sharp rise in fuel prices and the proposed removal of the capital gains tax discount has Australian households unusually worried about the future. This is important context for investors. Consumer sentiment often provides an early read on household spending, housing demand, inflation pressure, and the consumer sector’s earnings outlook.

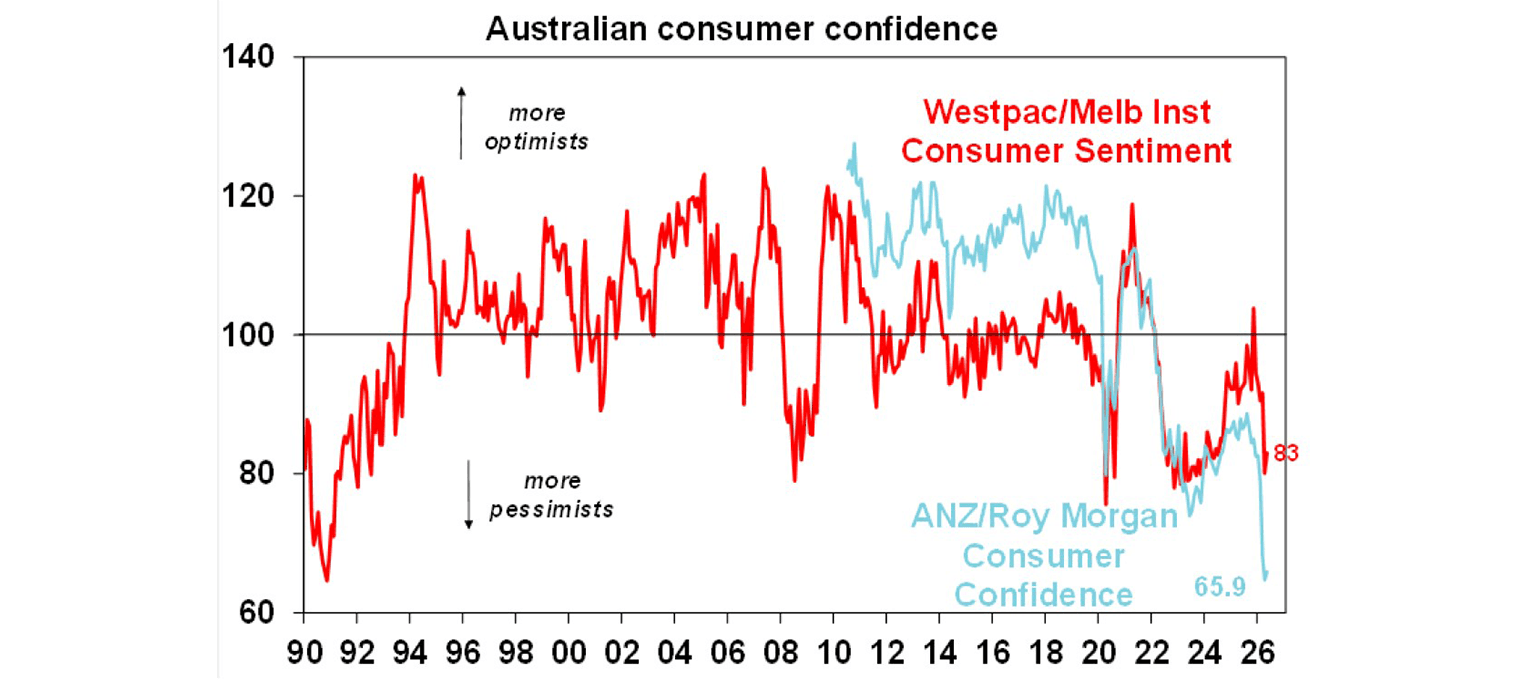

Consumer Sentiment Deeply Pessimistic

To the data. The latest Westpac–Melbourne Institute Consumer Sentiment Index rose 3.5% in May to 83, up from 80.1 in April.

Source: AMP

That’s a minor improvement, but it remains a deeply pessimistic reading. The story behind the data is that while some of April’s fuel price shock has eased, the benefit was largely offset by another RBA rate rise, and negative reactions to the Federal Budget’s proposed removal of the capital gains tax discount. In short, the household sector remains under pressure.

Explore 100's of investment opportunities and find your next hidden gem!

Search and compare a purposely broad range of investments and connect directly with product issuers.

A Cautious Signal About What’s Coming

A consumer sentiment reading below 100 generally points to pessimists outnumbering optimists. At 83, the index is telling us that households are very cautious about their finances right now. Moreover, expectations for the Australian economy over the next one and five years deteriorated, with the combined read at its weakest since November 2022. That highlights just how worried Australians are about the direction of the economy.

Why Investors Should Care

Consumer sentiment is a useful signal because household spending is a major driver of the Australian economy. When consumers are cautious, they tend to delay large purchases, trade down on discretionary spending, and prioritise mortgage repayments, rent, utilities, groceries and insurance. That’s likely to impact listed retailers, banks, consumer services companies, property-exposed businesses, and the service sector. It’s also likely to affect the country’s broader earnings cycle.

Rates Remain the Pressure Point

The May survey also pointed to a relatively challenging interest rate backdrop. Westpac reported that 85% of consumers still expected mortgage rates to rise over the next 12 months. That’s significant because rate expectations influence behaviour before actual rate changes are implemented. If households expect higher mortgage repayments, they may spend more cautiously today. Households are right to be cautious. The RBA remains hawkish, despite having space to wait and see, as they are concerned that inflation expectations could become embedded after several years of inflation running above their 2-3% target.

This backdrop has translated into more upward pressure on Australian bond yields than most other developed markets.

A Widening Generational Divide

One of the more interesting findings of the recent consumer sentiment release was the widening sentiment gap between younger and older consumers. Sentiment among baby boomers and Generation X was extremely weak, with index readings just below 70. Millennials were less pessimistic at 94.6, while Generation Z was outright positive at 104. Moreover, older cohorts were more likely to see the Budget as negative for their finances, while younger consumers were comparatively more positive about it. Hence, a more nuanced interpretation of consumer sentiment is warranted since different age groups drive different parts of the economy. Older households may be more exposed to retirement income, tax-efficient investment strategies, and residential property. Younger households may be more focused on paying rent, wage inflation, first-home affordability, and long-term wealth accumulation.

Subscribe to InvestmentMarkets for weekly investment insights and opportunities and get content like this straight into your inbox.

Portfolio Takeaways

The consumer sentiment data points to an economy that’s constrained. The consumer is cautious, rates are biting, inflation remains a risk, and the Budget has produced uneven effects across various age groups. For investors, the practical takeaways are:

- Avoid relying too heavily on a single macro outlook.

The Australian economy is sending mixed signals. Employment remains relatively resilient, inflation is proving sticky, consumer confidence is weak, and the RBA remains cautious. That creates a wider range of potential outcomes than investors have faced in recent years. A soft landing remains possible, but so do higher-for-longer interest rates, weaker consumer spending, slower economic growth, or renewed inflation pressures. External risks, including geopolitical tensions and commodity market volatility, add further uncertainty. Rather than positioning your portfolio around a single economic forecast, investors are likely to benefit from diversification across regions, asset classes, sectors, and investment styles. Rarely has the argument in favour of investing globally been stronger.

- Check fund and ETF exposure to the consumer sector.

In this environment, companies with pricing power, recurring revenue, contracted income streams, or exposure to essential services may prove more resilient than businesses reliant on discretionary spending and strong consumer demand.

So, investors in Australian equity funds and ETFs should look beyond headline index performance and examine the underlying sector exposures and how sensitive they are to consumer spending.

- Be selective with income assets.

Higher interest rates have improved yields across many income-producing investments, but not all income assets carry the same risks. In some cases, higher yields simply reflect higher levels of risk. With economic uncertainty elevated and consumer confidence weakening, the focus should be on the sustainability and quality of income rather than maximising yield alone. Investors should look beyond headline yields and assess factors such as duration risk, credit quality, liquidity, diversification, and fee structures. A diversified income allocation can help improve portfolio resilience across a range of potential economic outcomes.

- More due diligence of property-related exposures is warranted.

The survey’s homebuyer sentiment reading fell sharply to deeply pessimistic levels, while consumer house price expectations softened but remained positive. That combination is telling. Consumers may still believe property prices can rise, but fewer feel comfortable buying. Higher rates, affordability pressures, and policy uncertainty are all weighing on buyer confidence. This doesn’t mean property exposure should be avoided. It means listed property funds, REIT funds, property ETFs, and mortgage funds should be carefully assessed with a view to leverage, asset quality, tenant demand, distribution sustainability and liquidity. In tougher market conditions like these, due diligence matters more than ever.

Consumer Sentiment Flashing Yellow

Consumer sentiment is a useful warning light. Right now, it’s flashing yellow, weighed down by the Australian consumer sector’s pessimism. While it doesn’t bode well, the future remains uncertain. The next economic clues will come from retail sales, employment data, inflation, RBA commentary, mortgage stress indicators, and company earnings updates. The prudent investment response is to diversify globally, and make sure your portfolio matches your risk tolerance, liquidity needs, and time horizon.

Disclaimer: This article is prepared by Simon Turner. It is for educational purposes only. While all reasonable care has been taken by the author in the preparation of this information, the author and InvestmentMarkets (Aust) Pty. Ltd. as publisher take no responsibility for any actions taken based on information contained herein or for any errors or omissions within it. Interested parties should seek independent professional advice prior to acting on any information presented. Please note past performance is not a reliable indicator of future performance.

Author

Simon Turner

Head of Content (CFA)

Related Articles

-6gjpzrmfub3sdknjzdoy.jpg)

-r1k3iz2wqigm8nhwme1m.png)

Recent Articles

View all articles-ulhzagvbsmdk2tc72zgj.png)

-weh3swd4zyleexypgsv3.png)

-zdalarekmzl2x534cuyn.png)