-l7rg6lkopgoa2x6pxhua.png)

The Wild West Investor: Three Portfolio Pillars for an Uncertain Future

For decades, investors relied on the classic 60/40 portfolio: 60% equities and 40% bonds. That worked well during an era characterised by declining interest rates and relatively stable inflation.

However, the world has changed since then.

In a word, inflation has returned.

When inflation becomes the dominant economic force stocks and bonds can fall together, which arguably devalues the thinking behind the 60/40 portfolio. In 2022, one of the worst years for diversified portfolios in decades, both asset classes suffered significant declines as inflation surged and interest rates rose sharply.

The upshot is that the assumption that bonds will reliably offset equity losses is now less certain. Investors may need additional tools to achieve portfolio resilience in an inflationary world.

Why Traditional Diversification Is Being Tested

Diversification works well when portfolio assets respond differently but predictably to various economic scenarios.

For example, historically:

- Equities performed best during periods of rising economic growth.

- Bonds often performed well during economic slowdowns.

- The negative correlation between stocks and bonds helped smooth through-the-cycle returns.

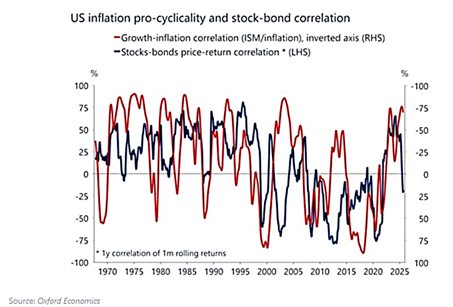

The more recent challenge is that correlations aren’t fixed, and are often unpredictable.

During inflationary shocks, stocks and bonds can become positively correlated, meaning both may decline simultaneously, as shown in the higher blue line readings below.

Inflation uncertainty is one of the key drivers behind these shifts in correlation behaviour.

This is why it’s time to look beyond a simple stock-and-bond portfolio allocation strategy to build resilience across multiple possible futures.

Hence, it’s worth thinking about portfolio construction in terms that match with the current lay of the land.

Introducing the three pillars of resilience:

Pillar One: Profitable Equities

As has been the case for many years, equities remain the primary engine of long-term wealth creation.

Businesses that generate consistent profits, possess pricing power and own valuable assets tend to outperform over extended periods. They can compound their earnings, grow their dividends, and adapt to changing economic environments.

However, investors should recognise that not all equities are created equal.

Periods of speculative enthusiasm can push valuations to unsustainable levels. Some sectors become crowded trades, while others remain overlooked.

For example, the AI trade has become frothy of late while precious metals have underperformed.

Rather than chasing market excitement at the more speculative end of the market, investors may benefit from focusing on diversified funds and ETFs invested in quality businesses trading at reasonable valuations.

Quality, profitable equities tend to perform best during periods of disinflationary growth, productivity expansions, technological innovation cycles, and stable economic conditions.

No other asset class has historically matched equities, particularly US equities, for long-term wealth generation.

The challenge is ensuring you are sufficiently diversified when US equities appear to be the only investment game in town. Like now.

Diversification is of most value when growth-focused asset classes are overextended.

Pillar Two: Commodities, Producers & Hard Assets

This is the pillar many portfolios are underweight.

Importantly, commodities, precious metals, energy producers and other hard assets often behave differently from both stocks and bonds. They have historically exhibited relatively low correlation with traditional financial assets and can provide diversification benefits during inflationary periods. Their performance is frequently driven by supply constraints, inflation pressures and geopolitical developments.

Consider the environments where commodities typically outperform: rising inflation, energy shortages, supply-chain disruptions geopolitical conflict, and stagflation.

These are precisely the environments where both stocks and bonds can struggle.

This doesn’t mean investors should move aggressively overweight commodities funds and ETFs. Commodity markets can be volatile and cyclical.

But this pillar can serve as a useful allocation that responds differently from the rest of the market when inflation becomes the dominant economic force.

Pillar Three: Cash and Short-Duration Fixed Income

Cash rarely makes it to the news headlines.

It’s often criticised during bull markets and ignored when risk assets are rallying.

Yet cash-equivalents play a valuable role in resilient portfolios.

Unlike long-duration bonds, cash and short-term fixed-income securities have limited sensitivity to rising interest rates. They also provide liquidity when opportunities emerge.

Many investors group all fixed income funds together, but a short-duration bond fund behaves very differently from a 20-year government bond fund.

The benefits are compelling. Short duration bond funds and cash-equivalents can provide liquidity during market stress, reduced interest-rate risk, portfolio stability, an capital for future opportunities.

These advantages are particularly valuable during periods of market stress when other investors are reacting to their emotions.

After all, it’s a lot easier to maintain a calm, proactive strategy when you’ve got cash on hand to take advantage of lower prices.

Key Takeaways for Investors

- Traditional 60/40 portfolios remain useful but may be less effective during inflationary shocks.

- Stock-bond correlations can change significantly depending on economic conditions.

- Commodities and hard assets can improve portfolio diversification because they often respond differently to inflation and supply shocks.

- Cash and short-duration fixed income can provide liquidity and stability during periods of market stress.

A Portfolio Built for Multiple Futures

One thing’s for sure: no one knows exactly what the future looks like.

The attraction of this three-pillar framework is that it acknowledges the inherent uncertainties in investing, particularly the risks created by the recent return of higher-for-longer inflation.

Each pillar responds differently to different economic conditions.

Quality, profitable equity funds and ETFs are likely to outperform in a disinflationary global growth scenario.

Commodities and hard assets are likely to outperform in an inflationary stagflation scenario.

Short duration fixed income and cash equivalents are likely to outperform during a market stress scenario involving tighter credit conditions.

Resilience is the name of the game.

Disclaimer: This article is prepared by Simon Turner. It is for educational purposes only. While all reasonable care has been taken by the author in the preparation of this information, the author and InvestmentMarkets (Aust) Pty. Ltd. as publisher take no responsibility for any actions taken based on information contained herein or for any errors or omissions within it. Interested parties should seek independent professional advice prior to acting on any information presented. Please note past performance is not a reliable indicator of future performance.

Author

Simon Turner

Head of Content (CFA)

Related Articles

-4jjuh9ocumc2do1vonr2.png)

-8c4ntrkc5xpa1bncy14s.jpg)

Recent Articles

View all articles-ulhzagvbsmdk2tc72zgj.png)

-weh3swd4zyleexypgsv3.png)

-zdalarekmzl2x534cuyn.png)